Champagne and supercars. Handbags and holidays. Watches and whisky. All of these form part of a €1.5 trillion global luxury goods industry1 – one that continues to evolve in response to shifting consumer preferences, cultural forces and economic pressures.

The luxury industry is almost unanimously associated with quality, exclusivity and prestige. While some may emphasise premium status, the appeal of luxury goods or services goes beyond this. Indeed, luxury brands tend to evoke strong emotions and associations that stem from decades, or even centuries, of established craftmanship and heritage, which come together to create an inherent and resilient brand value. Beyond exceptional quality and status, luxury therefore offers something else for the consumer: lifestyle appeal.

The luxury sector is broad, encompassing ‘hard’ luxury, such as watches and jewellery, and ‘soft’ luxury, like leather goods or clothing. Companies also range widely in size. At one end of the scale there is LVMH (Louis Vuitton, Moet & Hennesy) and Kering (Gucci, Saint Laurent & Bottega Veneta), which are fashion conglomerates that own multiple brands across a range of luxury product types. There are also independent fashion houses, such as Hermès in France or Burberry in the UK, which sell products across various ranges but all under the same brand. While luxury spans products, experiences and services, this article will focus predominantly on tangible goods.

If you studied economics, you’ll have learnt about supply and demand dynamics for goods and services. This lesson is often best illustrated through the impact that a change in price is expected to have on demand. For typical goods or services, you’d normally expect that as the price rises, demand subsequently falls. However, within luxury goods the opposite effect can take place. As the price of certain luxury goods or services increases, desirability and demand paradoxically increase. The economist accredited with this theory, Thorstein Veblen, introduced the idea of conspicuous consumption – spending money on luxury items to publicly display wealth or your social status.

To capitalise on this concept, luxury goods companies must carefully curate demand whilst also controlling and/or limiting supply. As tempting as it might be for a company to simply produce and sell more goods to grow, perceived exclusivity could be lost as a product or service becomes more widely available, thereby diminishing its desirability. Hermès, the French luxury goods company, has been successful in executing this strategy with their infamously scarce Birkin bag. This handbag is not held in stock in their stores; rather you are invited to buy the bag after making sufficient qualifying purchases on other goods. This approach is also utilised by Ferrari, where certain very high-end car models are only available by invitation to existing loyal customers. In both instances the scarce supply of these high-end products further strengthens their desirability.

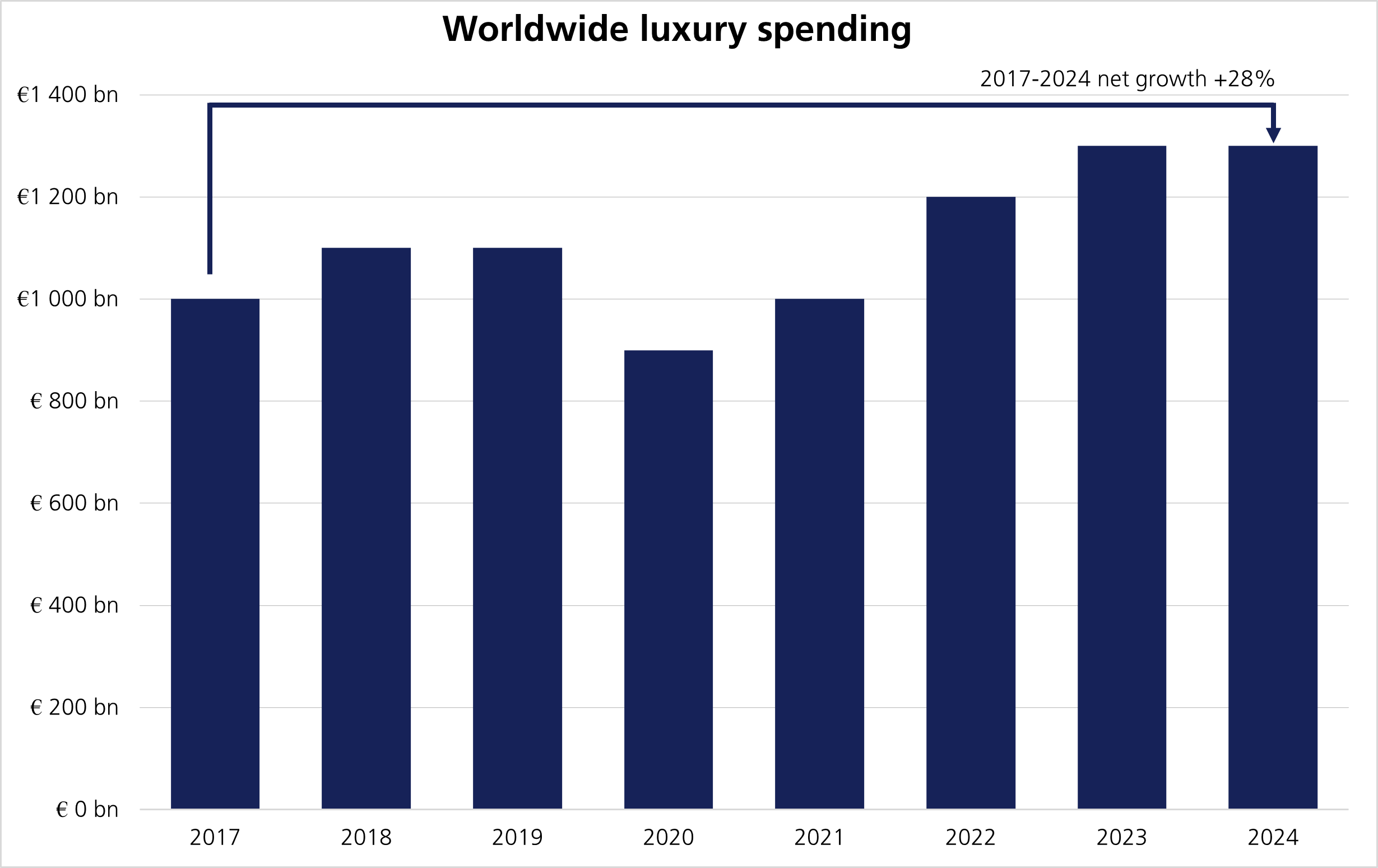

A key driver of growth for luxury goods companies comes from the rising middle class. As global wealth broadly increases, more and more people have higher levels of disposable income and/or wealth to spend. Evidence shows that as people become wealthier, their propensity to spend on luxury increases. Over the past decade this growing middle class has been most pronounced in developing countries, particularly China. From 2010 to 2024 it is estimated that Mainland China was the fastest growing region, posting an impressive +12% annualised growth in luxury goods sold.2 A little way behind in second place was the rest of world region, which posted an +8% annualised growth rate. Although emerging markets have provided faster growth for luxury companies, the mature European and North American markets still accounted for ~60% of 2024’s luxury good’s expenditure.

Recent years have not been without challenges. Several major luxury groups have experienced profit declines and share price volatility amid shifting global dynamics. Economic uncertainty, rising inflation and changing consumer sentiment, particularly among younger buyers, have led to more cautious spending in some regions. In the past couple of years, a number of listed luxury firms have reported softer-than-expected earnings. Kering (owner of Gucci) reported two years of negative organic growth, -2% in 2023 and -22% in 2024.3 These poorer results were attributed to weakness across Asia, but particularly China. The weakness in China also hurt LVMH and, to a lesser extent, Richemond Group (owner of Cartier). Whilst long-term fundamentals may remain intact, the short-term picture has reminded investors and brands alike that even the most prestigious names are not immune to cyclical headwinds.

Despite these challenges, the luxury sector continues to demonstrate resilience in certain areas, thanks mainly to strong brand value and an affluent customer base. Whilst certain brands have experienced negative growth across physical and online channels in recent years, outlet stores have seen increased traffic, posting positive growth of up to +3% in 2024 vs 2023.4 For luxury goods companies, the outlet channel not only provides an effective way to clear inventory but also serves as a more affordable entry point for new consumers, which works to expand their customer base.

The second-hand market also remains important for the sector as an effective pathway to attract new consumers. Both ‘hard’ and ‘soft’ luxury goods tend to hold their value over time thanks to both the perceived quality of the products and enduring brand value and, as second-hand retailers improve their certification processes to help ensure authenticity, consumer confidence continues to grow. This facilitates new consumers’ entry to luxury purchases, helping to create more loyal brand followers.

Within these markets, companies must continually evolve to remain relevant to the next generation of consumers. In recent years, ‘quiet’ luxury has emerged as a growing trend, characterised by a minimalist approach to fashion that emphasises thoughtful consumption, with a focus on so-called investment pieces. The trend eschews the idea of conspicuous consumption, as younger generations increasingly prefer understated (often logo-free) luxury that prioritises quality and craftsmanship, reflecting a broader cultural shift where discretion is valued over vanity. Another emerging theme is ‘sustainable luxury’, where consumers increasingly prioritise ethically sourced and environmentally friendly goods. This shift is most strongly associated with ‘Gen Z’ and ‘Millennials’, as they seek long-term and guilt-free ownership that aligns with their own values. Like all brands, luxury brands, will have to adapt to these shifting consumer preferences.

Another common consumer behaviour among the ‘next generation’ is their preference for spending on luxury experiences. This shift in consumer behaviour away from materialism and towards memorable experiences helps consumers gain more emotional fulfilment and status through access, not just objects. Luxury experiences can range from tailored or bespoke holidays and private dining with Michelin chefs to VIP access to art fairs, fashion shows or brand-hosted retreats – as just a few examples.

The luxury market has evolved and grown over multiple decades, and it remains an interesting and exciting sector. Companies in the industry must continually invest in their brands to ensure that desirability remains amongst their discerning consumer base. In addition to building their brands, management teams must also carefully control distribution to strike the optimal balance between short-term profits and long-term revenue growth. With the total addressable market set to grow over time, at LGT we continue to carefully monitor the underlying themes and trends to identify the companies we believe are best positioned to deliver strong financial performance.

Sources:

Luxury Report 2024: Rebuilding the Foundations of Luxury | Bain & Company

https://www.bain.com/insights/luxury-in-transition-securing-future-growth/

[1] Bain & Co 2024 Luxury Report

[2] Bain & Co 2024 Luxury Report

[3] Bloomberg

[4] Bain & Co 2024 Luxury Report

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority Registered in England and Wales: OC329392. Registered office: 14 Cornhill, London, EC3V 3NR. LGT Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Registered in Scotland number SC317950 at Capital Square, 58 Morrison Street, Edinburgh, EH3 8BP. LGT Wealth Management Jersey Limited is incorporated in Jersey and is regulated by the Jersey Financial Services Commission in the conduct of Investment Business and Funds Service Business: 102243. Registered office: Sir Walter Raleigh House, 48-50 Esplanade, St Helier, Jersey JE2 3QB. LGT Wealth Management (CI) Limited is registered in Jersey and is regulated by the Jersey Financial Services Commission: 5769. Registered Office: at Sir Walter Raleigh House, 48 – 50 Esplanade, St Helier, Jersey JE2 3QB. LGT Wealth Management US Limited is authorised and regulated by the Financial Conduct Authority and is a Registered Investment Adviser with the US Securities & Exchange Commission (“SEC”). Registered in England and Wales: 06455240. Registered Office: 14 Cornhill, London, EC3V 3NR.

This communication is provided for information purposes only. The information presented is not intended and should not be construed as an offer, solicitation, recommendation or advice to buy and/or sell any specific investments or participate in any investment (or other) strategy and should not be construed as such. The views expressed in this publication do not necessarily reflect the views of LGT Wealth Management US Limited as a whole or any part thereof. Although the information is based on data which LGT Wealth Management US Limited considers reliable, no representation or warranty (express or otherwise) is given as to the accuracy or completeness of the information contained in this Publication, and LGT Wealth Management US Limited and its employees accept no liability for the consequences of acting upon the information contained herein. Information about potential tax benefits is based on our understanding of current tax law and practice and may be subject to change. The tax treatment depends on the individual circumstances of each individual and may be subject to change in the future.

All investments involve risk and may lose value. Your capital is always at risk. Any investor should be aware that past performance is not an indication of future performance, and that the value of investments and the income derived from them may fluctuate, and they may not receive back the amount they originally invested.