It has been a tumultuous few years for British homeowners, who have seen their borrowing costs shoot up due to the Bank of England (BoE)’s attempts to curb inflation. Lately, the picture is looking a little brighter. In recent weeks, more banks have launched fixed mortgage deals below 4%, offering respite to homeowners locked in higher floating rates, or those looking to remortgage from higher fixed rates set several years ago.

Earlier this month, the BoE reduced rates by 0.25%, representing a cumulative reduction of 1% since interest rates peaked at 5.25% in August 2023. Many investors expect another two rate cuts this year, implying that the BoE will carry on with its one-cut-per-quarter pace. However, the debate around how far and fast rates will come down has been fluid as increasing global trade tensions muddy the outlook.

One of the key indicators influencing the BoE was the release of UK inflation data for April, which was published earlier this week. Although inflation had been cooling for several months, economists and the BoE forecasted higher inflation because of changes in utility bills and other annual price increases that are effective in April.

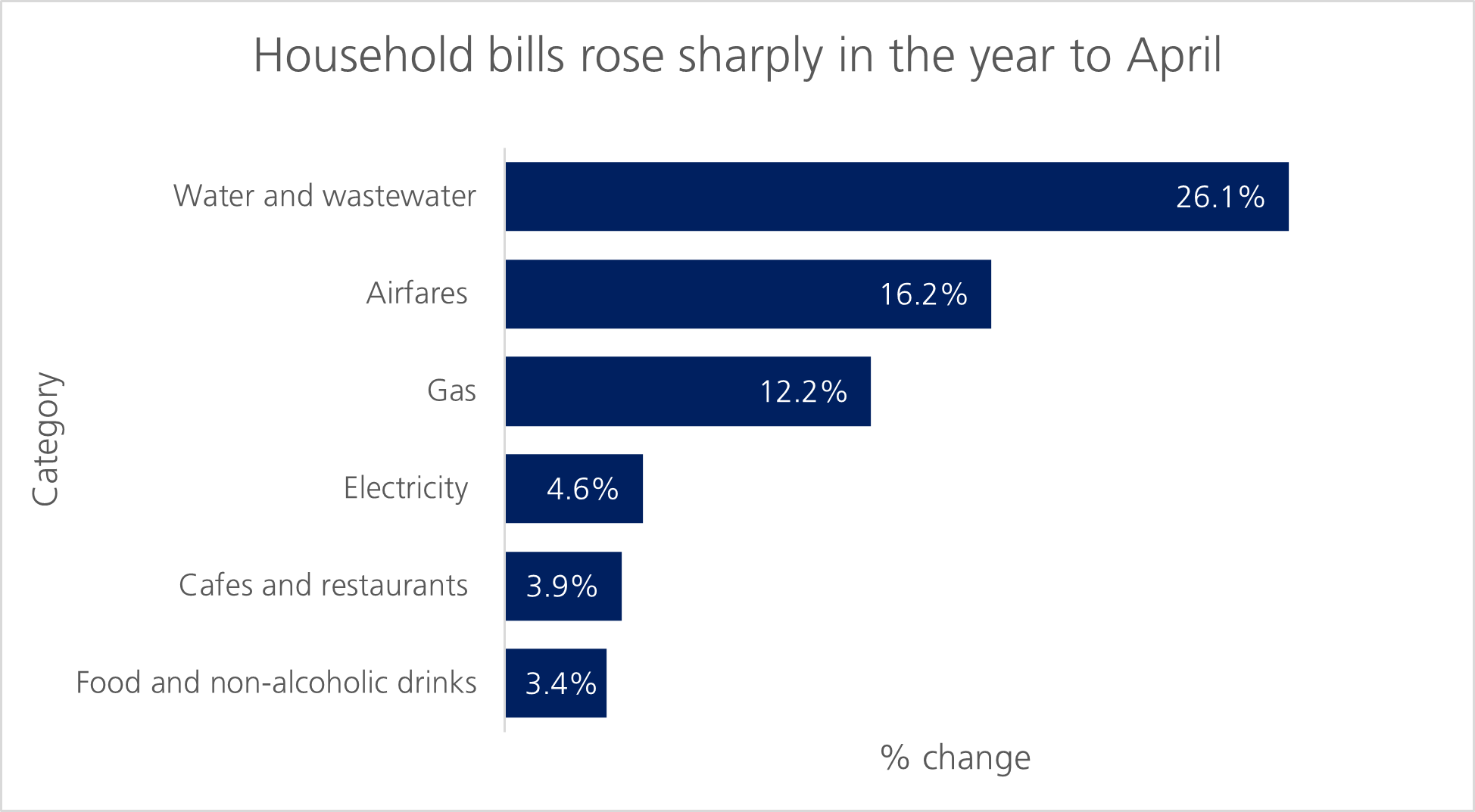

Factors impacting this latest CPI print are a staggering 26% rise in water bills; the new Office of Gas and Electricity Markets (Ofgem) price setting, which saw in April the annual bill for a household using a typical amount of gas and electricity rise to £1,849 per year, an increase of £1111; and increases in internet services and cable, cafes and restaurants and transportation/airfare.

Inflation from previous periods influences these numbers, which highlights the ripple effects of historical price increases. But this mix is further complicated by the timing of Easter this year, which led to higher flight costs over the school holidays in the UK.

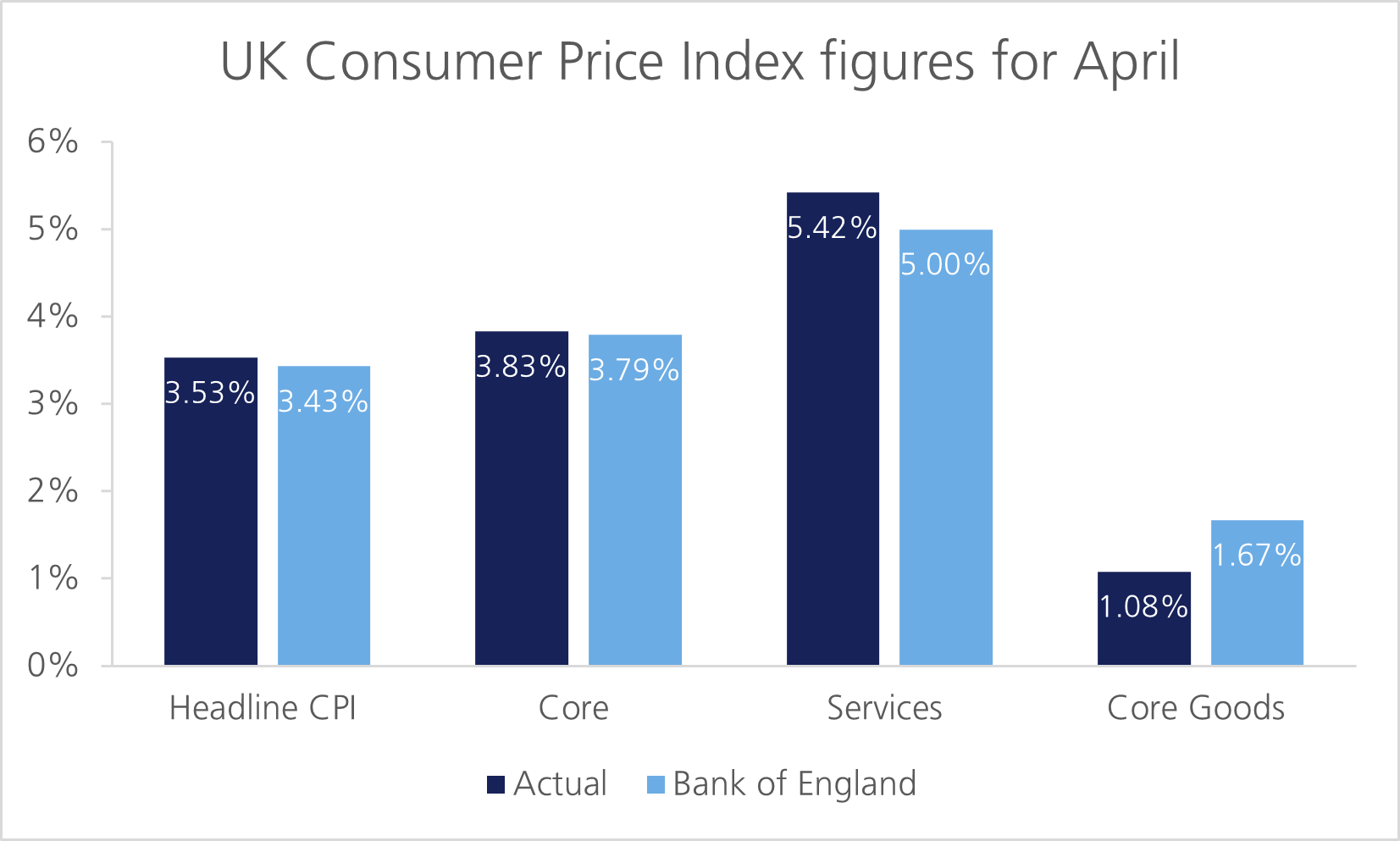

The increases in water, gas and electricity prices in April, along with a host of other bills, pushed inflation to 3.5% in April, up from 2.6% in March.2 The figures on a month-on-month basis meanwhile rose to 1.2% in April, relative to expectations of 1%.3 Core inflation—which excludes food and energy—and headline inflation experienced sharp increases, suggesting price increases across the board.

It is worth noting that the BoE has been predicting for some time that inflation would be higher in the summer of 2025 before gradually falling closer to its target level of 2% by mid-2026. In February, the BoE forecasted Consumer Price Index (CPI) inflation would hit 3.7% in the summer of 2025, but in its most recent report, revised projections to 3.4% in Q2 and 3.5% in Q3. So the actual figures are not far off the BoE’s original forecasts.

The key question now is whether this will alter the BoE’s interest rate path.

Huw Pill, chief economist at the BoE, said at a Barclays conference this week the “withdrawal of policy restriction has been running a little too fast of late, given the progress achieved thus far with returning inflation to target”. Pill, who opposed the quarter-point reduction earlier this month, advocated policymakers “skip” reducing rates rather than “halting” the process of lowering levels. “My starting point is that the pace of the Bank Rate reduction should be ‘cautious’, running slower than the 0.25% per quarter we have implemented since last August,” Pill said, as he justified his “courage not to act”.4

The BoE meanwhile stated that given the committee’s “evolving view of the medium-term outlook for inflation, a gradual and careful approach to the further withdrawal of monetary policy restraint remains appropriate.”5 Although labour data has been poor, resulting in the head of the Office for National Statistics (ONS), Sir Ian Diamond, resigning,6 the BoE’s own forecasts were not wildly off the mark.

The BoE should get more clarity from alternative data sources as well as official sources over coming quarters. However, despite the higher inflation figures for April, there are green shoots. The trade framework the UK has put in place with the US along with closer ties to Europe has provided more scope for deflationary forces to work their way into the economy. The UK’s efforts to ease trade barriers could lower costs and friction, potentially shifting the balance between growth and inflation favourably. In theory, this could enable the BoE to carry on with its slow and steady rate cutting cycle.

[1] BBC: https://www.bbc.com/news/articles/cdd29v8mp9jo

[2] ONS: https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/april2025

[3] ONS: https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/consumerpriceinflation/april2025

[4] Bank of England: https://www.bankofengland.co.uk/-/media/boe/files/speech/2025/may/the-courage-not-to-act-remarks-by-huw-pill.pdf

[5] Bank of England: https://www.bankofengland.co.uk/monetary-policy-report/2025/may-2025

[6] BBC: https://www.bbc.com/news/articles/cx2qnzdvq25o

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority Registered in England and Wales: OC329392. Registered office: 14 Cornhill, London, EC3V 3NR. LGT Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Registered in Scotland number SC317950 at Capital Square, 58 Morrison Street, Edinburgh, EH3 8BP. LGT Wealth Management Jersey Limited is incorporated in Jersey and is regulated by the Jersey Financial Services Commission in the conduct of Investment Business and Funds Service Business: 102243. Registered office: Sir Walter Raleigh House, 48-50 Esplanade, St Helier, Jersey JE2 3QB. LGT Wealth Management (CI) Limited is registered in Jersey and is regulated by the Jersey Financial Services Commission: 5769. Registered Office: at Sir Walter Raleigh House, 48 – 50 Esplanade, St Helier, Jersey JE2 3QB. LGT Wealth Management US Limited is authorised and regulated by the Financial Conduct Authority and is a Registered Investment Adviser with the US Securities & Exchange Commission (“SEC”). Registered in England and Wales: 06455240. Registered Office: 14 Cornhill, London, EC3V 3NR.

This communication is provided for information purposes only. The information presented is not intended and should not be construed as an offer, solicitation, recommendation or advice to buy and/or sell any specific investments or participate in any investment (or other) strategy and should not be construed as such. The views expressed in this publication do not necessarily reflect the views of LGT Wealth Management US Limited as a whole or any part thereof. Although the information is based on data which LGT Wealth Management US Limited considers reliable, no representation or warranty (express or otherwise) is given as to the accuracy or completeness of the information contained in this Publication, and LGT Wealth Management US Limited and its employees accept no liability for the consequences of acting upon the information contained herein. Information about potential tax benefits is based on our understanding of current tax law and practice and may be subject to change. The tax treatment depends on the individual circumstances of each individual and may be subject to change in the future.

All investments involve risk and may lose value. Your capital is always at risk. Any investor should be aware that past performance is not an indication of future performance, and that the value of investments and the income derived from them may fluctuate, and they may not receive back the amount they originally invested.