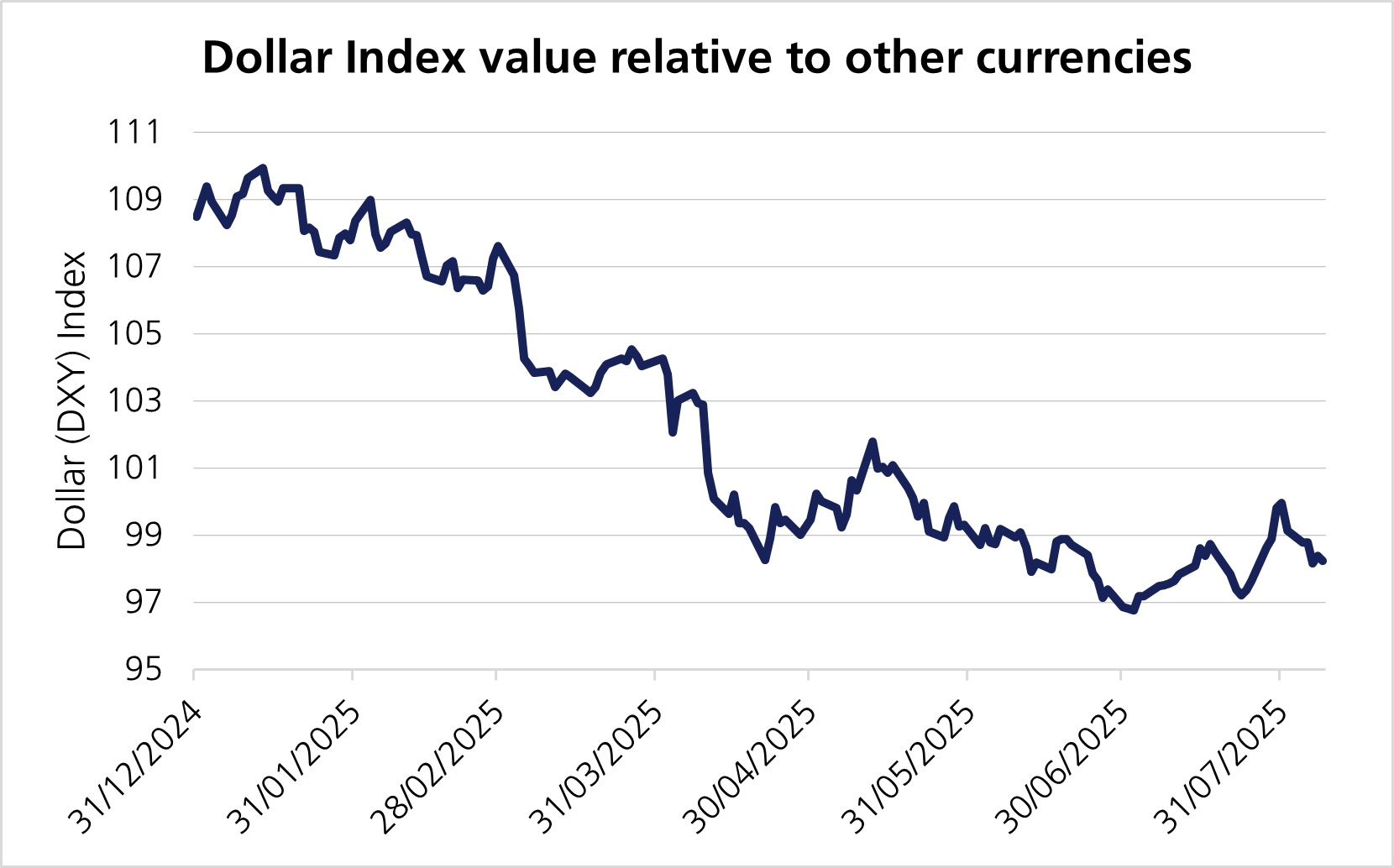

President Donald Trump’s chaotic rollout of tariffs has had an enormous impact across asset classes this year. But none have felt the impact as much as the dollar, which got off to its worst first half of the year in more than half a century. The greenback weakened by more than 10% in the first six months of the year. The last time the dollar registered such poor performance was in 1973, when the US stopped linking the dollar to the price of gold.1

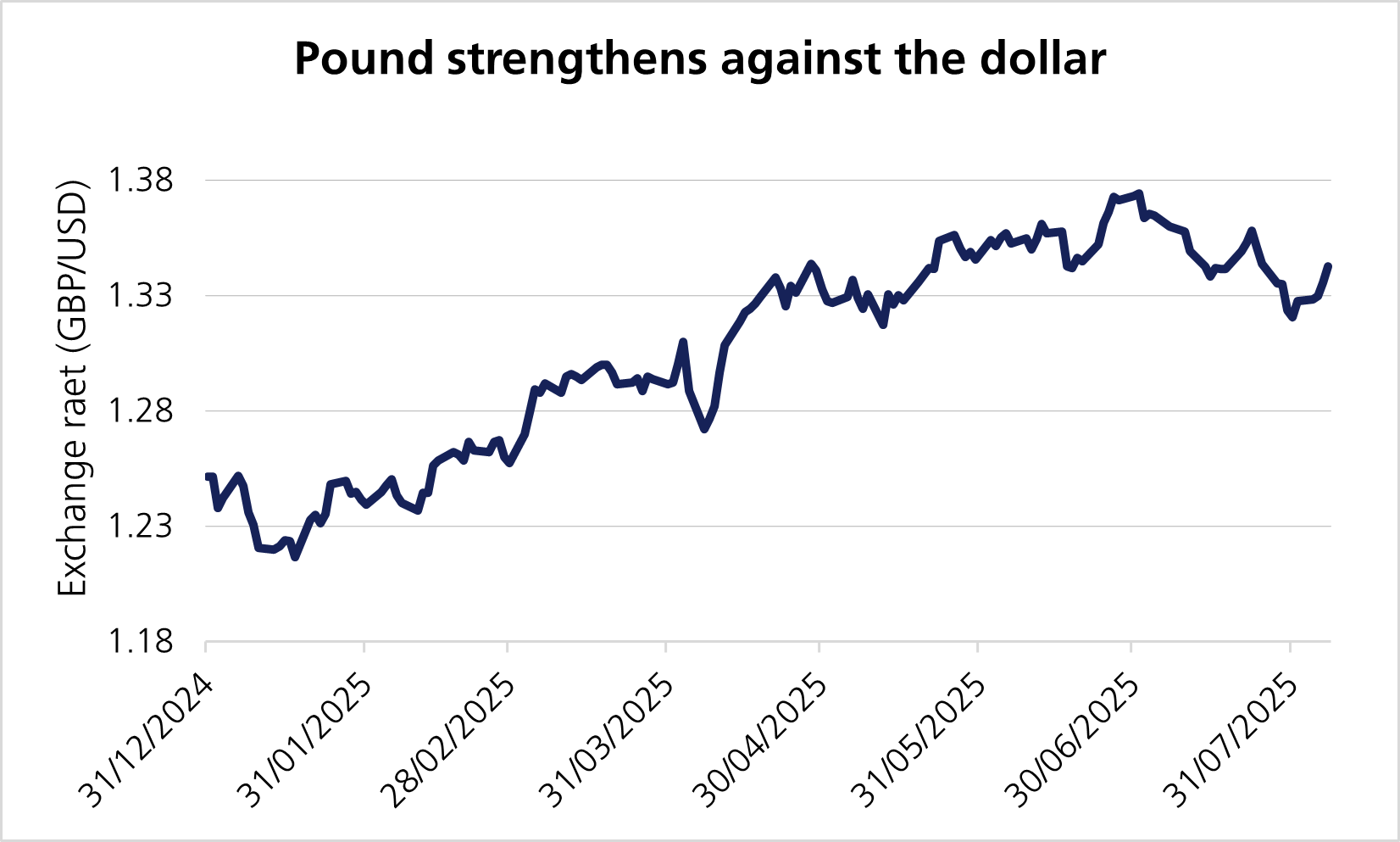

Dollar weakness this year is particularly stark when compared to the British pound, which has led some to argue this is a sign of relative strength in the UK economy or in sterling itself. This week we take a closer look at the cable trade this year – the exchange rate between the dollar and the pound – and delve into the dynamics at play for one of the world’s most traded pairs in foreign exchange (FX) markets.

The recent appreciation in the pound vs the dollar – seen with the euro, Australian dollar and others – is primarily driven by broad-based dollar weakness rather than any specific factors relating to the UK. Underlying macroeconomic data in the UK has remained subdued, with muted growth, persistent inflation pressures and cautious Bank of England (BoE) guidance about future rate cuts.

There are several key drivers that have weakened the dollar relative to a basket of currencies, which we outline below.

The first half of the year saw US GDP growth of around 1% on average, but most economists expect this to move down slightly in coming quarters over uncertainty about how tariffs will weigh on business capex and the end consumer. Meanwhile the core PCE (Personal Consumption Expenditures) index – the Federal Reserve (Fed)’s preferred inflation gauge – came closer to the Fed’s target of 2%, reaching 2.7% in May. Although it is still too early to assess the tariff impact on inflation, most economists believe the impact will become evident in the next few years, keeping inflation persistently above the Fed’s target.2

There has also been a shift in market expectations of future Fed rate cuts, with markets increasingly pricing in the chances of a Fed cut at its next meeting in September following recent weaker-than-expected jobs report.3 The Fed’s policymaking arm, the Federal Open Market Committee (FOMC), has remained steadfast against lowering interest rates for some time – inflation remains above the Fed’s 2% target rate, and Fed Chairman Jerome Powell has said the Fed is waiting to see how tariffs will impact inflation before considering more cuts. But the softer-than-expected jobs report on 1 August – which weighed on the dollar further – has also led markets to price in a 90% chance of a rate cut at the Fed’s September meeting.4

The US fiscal situation continues to deteriorate, with the Senate passing Trump’s so-called “big, beautiful bill”, a bill that will substantially raise the US deficit levels. Some economists are forecasting this package of tax cuts will elevate the deficit to 6.5% to 7% of GDP over the next few years5 and could add an estimated $3.3 trillion to the national debt over 10 years.6 This increased debt means the US government will issue more Treasuries, but investors are concerned over the US government’s ability to repay this substantial debt. This in turn has led to a loss in confidence in not only US Treasury markets, but in the dollar itself as investors rotate into other asset classes as global risk appetite improves.

Global investors have been increasing their outright US dollar exposure over the past decade. Despite global money managers’ and pension funds’ obligations in local currencies, they have been reluctant to hedge their dollar, primarily because the dollar has acted as a natural hedge for their portfolios – when markets fell, the dollar appreciated. However, since the start of this year, a softening dollar has adversely impacted returns for foreign investors in US assets. As a result, foreign investors have started hedging more of their portfolio. And since the dollar declined along with US risk assets, it lost its natural hedging protection. This ultimately encouraged more investors to hedge.

So the recent pound appreciation against the dollar is primarily a story about the weakening dollar, rather than about the state of the UK economy or policy.

Whilst there is no doubt that the rally in the dollar over the past few years has resulted in an overvalued greenback, we do believe the recent weakness mentioned above may slow and even reverse in the next six-to-12 months. Tariff concerns subsiding, strong US corporate earnings growth relative to other developed markets, and expectations that the US economic growth will outpace other developed markets all suggest that the pace of the weakening dollar may slow or even stop, resulting in a more range bound dollar/sterling rate.

The UK meanwhile remains exposed to several structural and cyclical challenges that could weigh on sterling, such as political uncertainty, subdued productivity and less policy flexibility.

It is important to remember that equity markets are efficient, and global companies’ share prices are influenced by currency movements. If the dollar does continue to weaken against the pound, share prices of some companies, such as Apple, could experience a boost as their overseas earnings in dollar terms would go up. Currencies are difficult to predict, but demonstrate good mean reverting characteristics, meaning they tend to return to a long-term average or equilibrium level after periods of divergence.

At LGT, our philosophy is to keep our equity exposure unhedged. However, we do closely monitor portfolio exposure and sensitivity to FX moves. We believe in the long-term growth potential of equity markets and view short-term volatility as an opportunity to buy quality assets at discounted prices. By remaining unhedged, we stay fully aligned with the market’s natural growth trajectory, allowing us to better capture the upside. That is not to say we do not take advantage of extreme currency moves – we hedged part of our dollar exposure during the Liz Truss debacle when we believed the pound was oversold.

[1] NYTimes: The Dollar Has Its Worst Start to a Year Since 1973

[2] JPMorgan: Macro & Markets Midyear Outlook

[3] Forbes: Fed Expected To Cut Interest Rates In September

[4] Deutsche Bank

[5] Deutsche Bank

[6] BBC: The key items in Trump's 'big, beautiful bill'

LGT Wealth Management UK LLP is authorised and regulated by the Financial Conduct Authority Registered in England and Wales: OC329392. Registered office: 14 Cornhill, London, EC3V 3NR. LGT Wealth Management Limited is authorised and regulated by the Financial Conduct Authority. Registered in Scotland number SC317950 at Capital Square, 58 Morrison Street, Edinburgh, EH3 8BP. LGT Wealth Management Jersey Limited is incorporated in Jersey and is regulated by the Jersey Financial Services Commission in the conduct of Investment Business and Funds Service Business: 102243. Registered office: Sir Walter Raleigh House, 48-50 Esplanade, St Helier, Jersey JE2 3QB. LGT Wealth Management (CI) Limited is registered in Jersey and is regulated by the Jersey Financial Services Commission: 5769. Registered Office: at Sir Walter Raleigh House, 48 – 50 Esplanade, St Helier, Jersey JE2 3QB. LGT Wealth Management US Limited is authorised and regulated by the Financial Conduct Authority and is a Registered Investment Adviser with the US Securities & Exchange Commission (“SEC”). Registered in England and Wales: 06455240. Registered Office: 14 Cornhill, London, EC3V 3NR.

This communication is provided for information purposes only. The information presented is not intended and should not be construed as an offer, solicitation, recommendation or advice to buy and/or sell any specific investments or participate in any investment (or other) strategy and should not be construed as such. The views expressed in this publication do not necessarily reflect the views of LGT Wealth Management US Limited as a whole or any part thereof. Although the information is based on data which LGT Wealth Management US Limited considers reliable, no representation or warranty (express or otherwise) is given as to the accuracy or completeness of the information contained in this Publication, and LGT Wealth Management US Limited and its employees accept no liability for the consequences of acting upon the information contained herein. Information about potential tax benefits is based on our understanding of current tax law and practice and may be subject to change. The tax treatment depends on the individual circumstances of each individual and may be subject to change in the future.

All investments involve risk and may lose value. Your capital is always at risk. Any investor should be aware that past performance is not an indication of future performance, and that the value of investments and the income derived from them may fluctuate, and they may not receive back the amount they originally invested.